The Link Between Bookkeeping and Taxation

The Importance of Good Bookkeeping

Good bookkeeping is the foundation of strong financial management. When your records are accurate and organized, you gain a clear picture of your income, expenses, and overall financial health. This clarity helps you make better decisions, avoid costly mistakes, and stay compliant with tax laws.

Accurate books also make tax season smoother, reducing the risk of errors, penalties, or missed deductions. Whether you’re an individual or a business owner, consistent bookkeeping is one of the smartest financial habits you can build.

Understanding the Basics of Taxation

Taxes affect everyone—individuals and businesses alike. The most common types include income tax, sales tax, property tax, and capital gains tax.

Income tax is based on your earnings and varies by tax bracket.

Sales tax applies to goods and services and differs by state or city.

Property tax is tied to the value of your real estate and funds local services.

Capital gains tax applies when you profit from selling assets like stocks or property.

Knowing how these taxes work helps you plan better and avoid surprises.

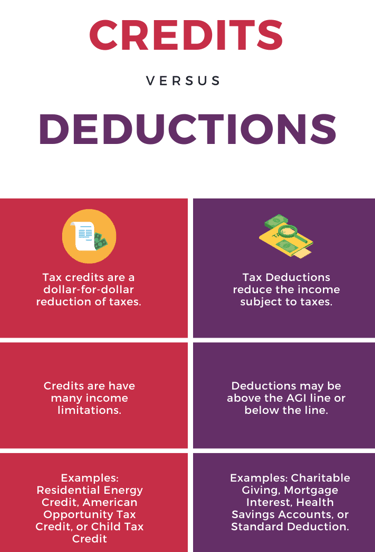

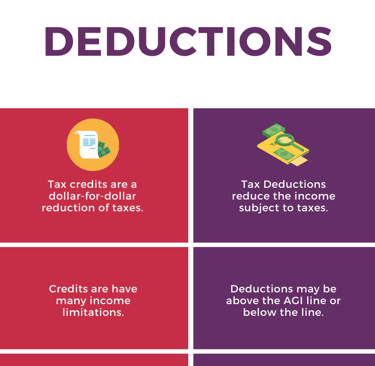

Deductions vs. Credits: What’s the Difference?

Tax deductions and tax credits both reduce your tax bill, but they work differently:

Deductions lower your taxable income.

Credits reduce the tax you owe dollar for dollar.

Understanding which ones you qualify for can significantly reduce your tax liability. Good bookkeeping ensures you don’t miss opportunities to save.

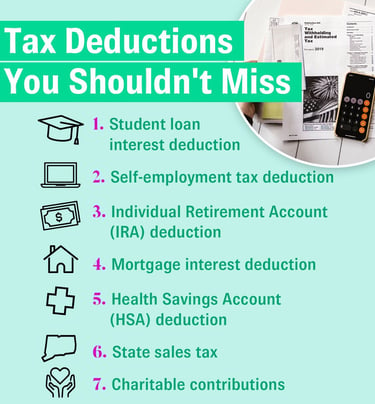

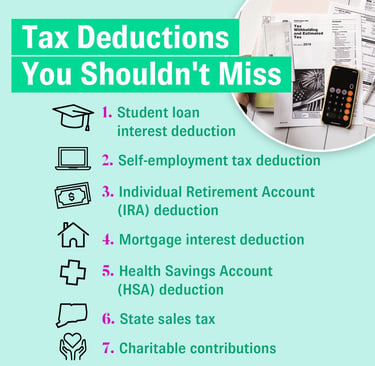

Common Tax Deductions for Individuals

Many taxpayers miss out on deductions they’re eligible for. Some of the most common include:

Mortgage interest

Medical expenses above a certain percentage of your income

State and local taxes

Charitable contributions

Keeping detailed records throughout the year makes claiming these deductions much easier.

Common Tax Deductions for Businesses

Businesses can reduce taxable income by deducting ordinary and necessary expenses such as:

Rent for office space

Employee salaries

Supplies and materials

Depreciation on equipment

Accurate bookkeeping ensures these expenses are properly tracked and documented.

Understanding Tax Credits

Tax credits can offer even bigger savings than deductions. Examples include:

Earned Income Tax Credit (EITC)

Child Tax Credit

Education credits

Energy‑efficient home credits

Credits directly reduce the amount of tax you owe, making them extremely valuable.

Best Practices for Accurate Financial Records

Strong bookkeeping starts with good habits:

Keep receipts organized (digital or physical).

Use accounting software like QuickBooks, FreshBooks, or Xero.

Reconcile your accounts monthly.

Maintain a separate bank account for business transactions.

These practices help prevent errors and make tax filing much easier.

Why Bookkeeping and Taxes Go Hand in Hand

Good bookkeeping leads to accurate tax returns. When your financial records are complete and organized:

You avoid penalties and interest.

You maximize deductions and credits.

You reduce stress during tax season.

You gain better control over your financial future.